Last Updated on 07/20/2026 by Ethan Sawyer

If you’re filling out the FAFSA, you might notice an unfamiliar term popping up: Student Aid Index, or SAI. Introduced as part of the FAFSA redesign for the 2024-25 school year, the SAI replaced the old Expected Family Contribution (EFC).

Why the change?

Because the EFC often misled students and families into thinking it was the exact amount they would have to pay out of pocket, which wasn’t true.

The Student Aid Index is a better guide. It’s a number that colleges and universities use to estimate your financial need and put together your aid package.

But SAI is still plenty unclear to a lot of students and families. So in this post, we’ll walk you through

-

what the SAI is

-

how it’s calculated

-

what it means for your college costs

-

your financial aid eligibility

-

and how to plan for what you might actually pay.

What is the Student Aid Index?

The Student Aid Index (SAI) is a number that colleges use to figure out how much financial aid you may be eligible for after you submit the FAFSA. It replaced the Expected Family Contribution (EFC) starting with the 2024-25 FAFSA to make things more straightforward for students and families.

The SAI can range from -1,500 to 999,999.

A lower number means you will likely qualify for more need-based aid, like grants and subsidized loans. If your SAI is negative or zero, you’re likely eligible for the maximum Pell Grant award.

How does the Student Aid Index work?

First, remember that your SAI is just a number. It’s not a bill or an amount you have to pay. Schools use it alongside your cost of attendance (COA), which includes things like tuition, fees, housing, meals, books, transportation, and other personal expenses.

Here’s how SAI works: After you fill out your FAFSA, the Department of Education reviews your (and often your parents’ or spouse’s, if you’re married) financial information, such as your/your family’s income and assets. Based on that, they calculate your SAI by subtracting the amount needed for your family’s normal living expenses from your reported income and assets.

Here’s the basic formula colleges use to figure out your financial need:

Cost of Attendance – Student Aid Index = Financial Need

To illustrate: Let’s say your school’s annual cost of attendance is $40,000, and your SAI is 0. That means, according to the FAFSA calculations, you have $40,000 of financial need. If your SAI is $5,000, then your financial need would be $35,000.

This number helps colleges decide how much need-based aid you may qualify for, including grants, scholarships, work-study jobs, and loans.

The SAI also plays a big role in determining your eligibility for federal aid, especially the Pell Grant (Speaking of, here’s a guide to Pell Grants). Pell Grants are designed for students with significant financial need. If your SAI is 0 or negative (the lowest possible SAI is -1,500), you’ll likely qualify for the maximum Pell Grant award. As your SAI gets higher, the amount of Pell Grant money you qualify for may go down.

Important to note: Even if you have a high financial need, colleges aren’t always required to meet 100% of it. Some schools cover the full gap between what you can afford and their cost, but many offer a mix of grants, loans, and work-study opportunities to help bridge the difference.

There are some schools that offer complete financial aid, though some do so with loans, and some without, so check that guide for more.

How SAI is calculated

The Student Aid Index is calculated using the information you (and your parents or spouse, if applicable) report on your FAFSA. Most of the time, your financial details (i.e., income and tax info) are pulled directly from the IRS into the FAFSA to make things easier.

Here’s what goes into the calculation:

-

Your family’s income (including taxable and untaxed income)

-

The net worth of any assets (like savings, investments, and real estate)

-

Your household size

The formula totals your available financial resources and then subtracts an amount for basic living expenses (called the Income Protection Allowance). What’s left over is what the government thinks could potentially go toward college costs, and that becomes your SAI.

One big change to know: The number of siblings you have in college no longer reduces your SAI, a shift from the old system. Also, for the first time, your SAI can be negative, which helps identify students with the greatest financial need.

How colleges use your SAI

Colleges use your SAI to decide how much financial aid they can offer you. After determining their cost of attendance for the year, the financial aid office subtracts your SAI and any other grants or scholarships you’re receiving to calculate your remaining financial need.

From there, they put together a financial aid package that may include:

-

Need-based grants

-

Scholarships

-

Federal student loans

-

Work-study opportunities

A lower SAI usually means you’ll qualify for more need-based aid. However, not every school can meet your full financial need. Some will cover a larger percentage of your financial need than others. That’s why comparing financial aid offers is important when making your college decision.

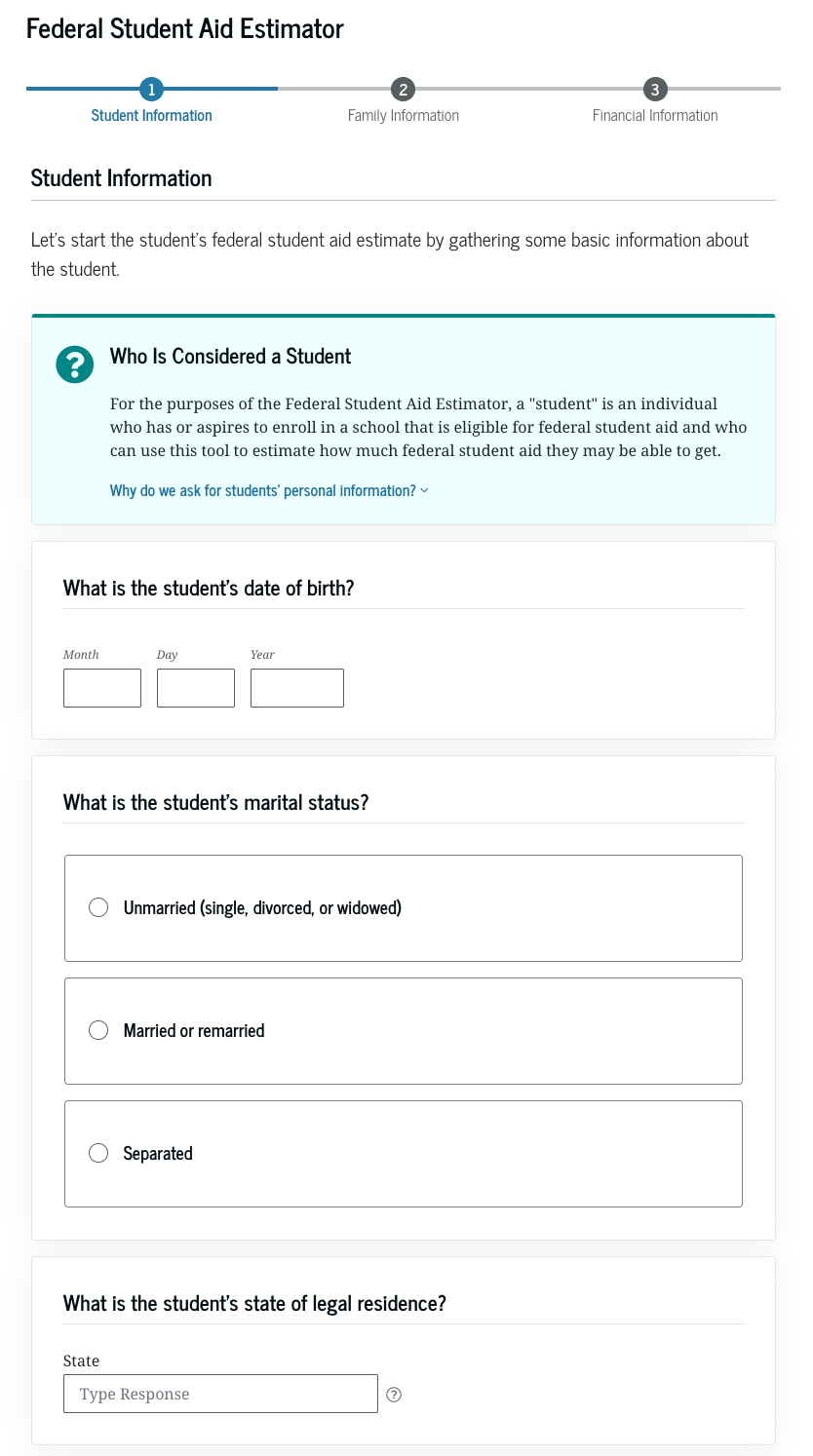

Estimated Student Aid Index

Wondering what your Student Aid Index might be before you even submit your FAFSA? You can get an early estimate using the Federal Student Aid Estimator, a free tool provided by the U.S. Department of Education.

The Federal Student Aid Estimator asks you a series of basic questions about your family’s income, assets, and household size. Based on your answers, it gives you an estimated SAI and a rough idea of the types of federal aid you might qualify for, including Pell Grants, federal loans, and work-study.

Use the Federal Student Aid Estimator to get an early estimate of your Student Aid Index and potential financial aid. (Image source)

It’s important to know that the estimate isn’t official. Your final, official SAI will only be calculated once you submit the FAFSA. But using the estimator can help you start planning.

If you’re early in your college search, using the estimator can also help you understand how different financial factors (like family income or savings) could impact your eligibility for aid. That way, you can make more informed decisions about where to apply and what kind of financial support you might need.

Tip: After getting your estimated SAI, consider using net price calculators on individual college websites. These calculators factor in your estimated SAI and each school’s specific financial aid policies to better estimate your potential costs.

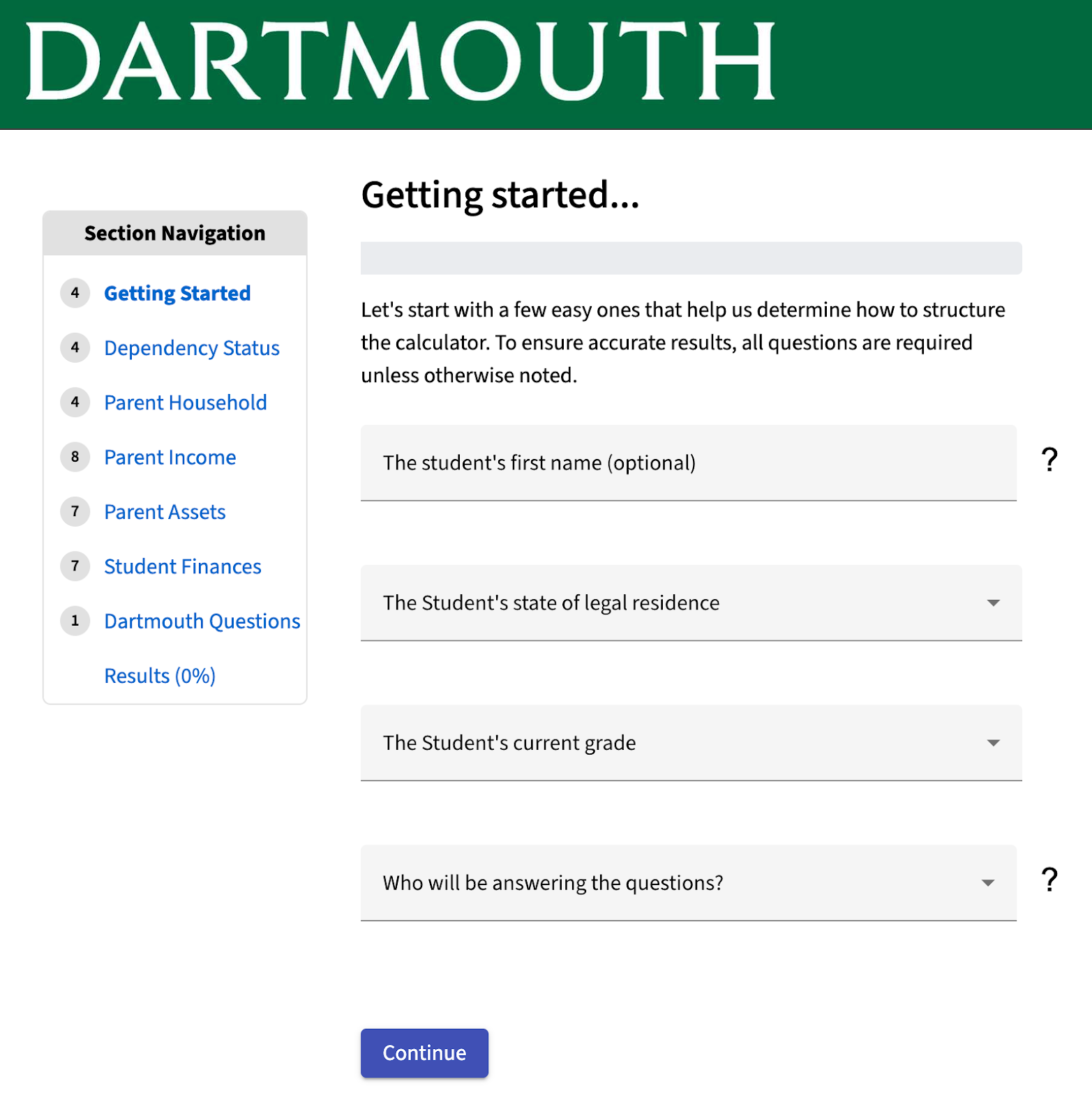

For example, here’s what Dartmouth’s looks like:

Many colleges offer net price calculators like this one to help you estimate your actual cost of attendance based on your financial information. (Image source)

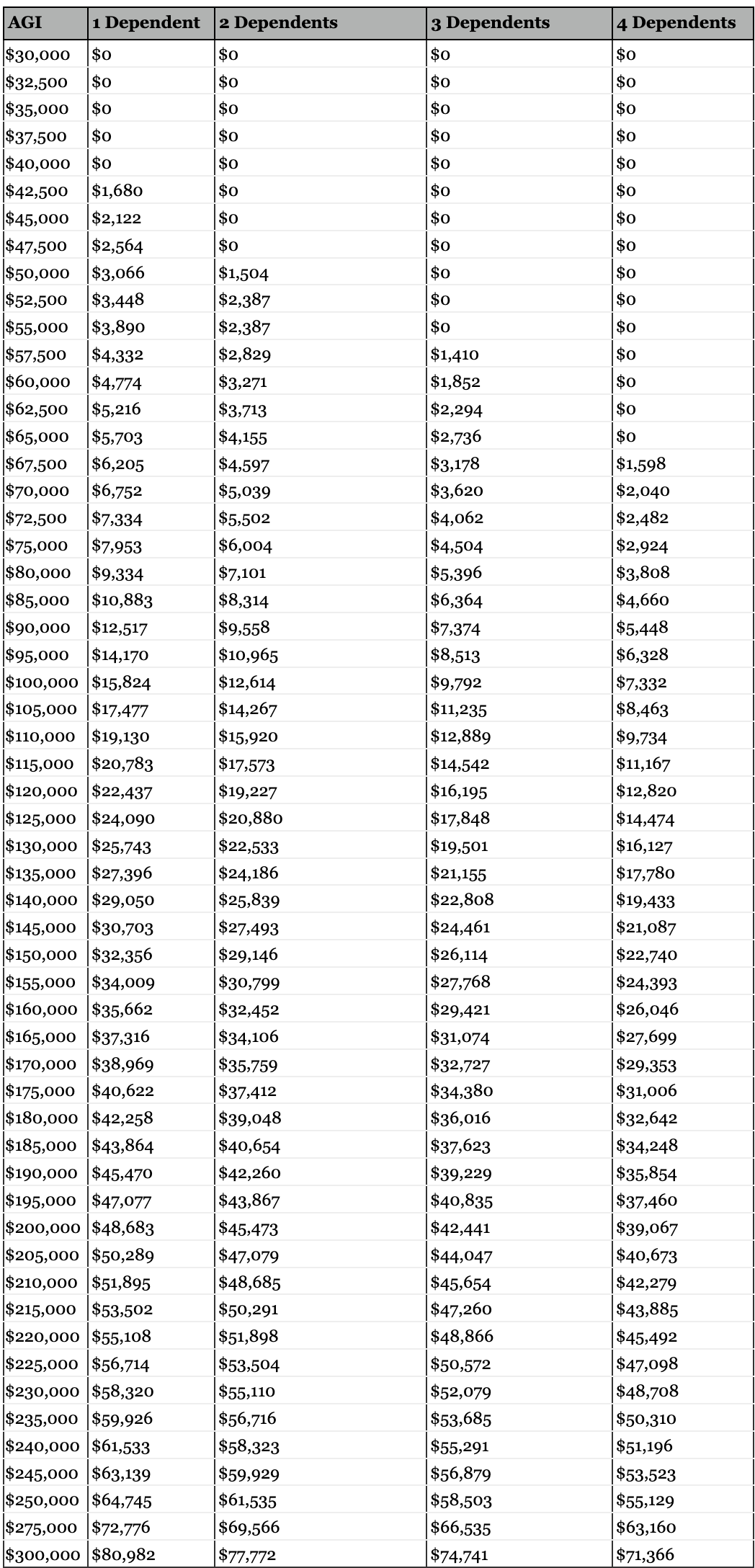

Student Aid Index chart

The chart below shows estimated Student Aid Index (SAI) values based on your family’s Adjusted Gross Income (AGI) and the number of dependents in your household. It can give you a rough idea of how much need-based aid you might qualify for before you submit the FAFSA.

FAQ on Student Aid Index

How do I find my Student Aid Index?

After you submit your FAFSA, you’ll receive a document called the FAFSA Submission Summary. Your official SAI will be listed there. This number is calculated based on the financial information you provided, and colleges use it to determine your eligibility for financial aid.

What if my estimated Student Aid Index is negative?

A negative SAI (as low as -1,500) is a good thing when it comes to financial aid, in that it means you’ll qualify for the close to the maximum amount of need-based aid, like the full Pell Grant. Some colleges may also offer additional institutional grants if they see that your need is especially high.

What is a high SAI?

A high SAI means that, based on your FAFSA information, the government estimates that you have more ability to pay for college. Students with higher SAIs are less likely to qualify for need-based federal aid but may still be eligible for merit scholarships or other non-need-based financial support.

What is a low SAI?

A low SAI means you have significant financial need. Students with low SAIs often qualify for the most generous need-based aid, like Pell Grants, subsidized federal loans, and sometimes additional aid from colleges to help cover remaining costs.

What is a “good” SAI?

Generally, a “good” SAI for students means a lower number. The lower your SAI, the more likely you are to qualify for grants, scholarships, and need-based aid. A negative or zero SAI often unlocks the maximum amount of federal aid available.

Can I challenge my SAI?

You can’t directly challenge your SAI with the federal government. Still, you can contact the financial aid offices at the colleges you’re applying to and submit a financial aid appeal letter. If you’ve experienced significant financial changes (like job loss or major medical expenses), the college’s financial aid department may adjust your financial aid package after a review.

Final thoughts

While the SAI might seem like just another number, it plays a significant role in shaping your financial aid package. It can also help you make smarter decisions about where to apply and what to expect financially.

Now that you know what the SAI is and how it works, your next step is to use tools like the Federal Student Aid Estimator and college net price calculators. These can give you a clearer picture of your potential aid before you even submit the FAFSA.

Want more advice on how to maximize your college financial aid? Check out this resource next: Crash Course on How to Pay for College (Using as Little of Your Own Money as Possible).

Ameer Drane is a freelance writer who specializes in writing about college admissions and career development. Prior to freelancing, Ameer worked for three years as a college admissions consultant at a Hong Kong-based education center, helping local high school students prepare and apply for top colleges and universities in the US. He has a B.A. in Latin American Studies from the University of Chicago and an M.A. in Spanish Linguistics from UCLA. When he’s not working, Ameer loves traveling, weight lifting, writing, reading, and learning foreign languages. He currently lives in Bangkok, Thailand.

Top values: Growth / Diversity / Empathy