Hello! You’ve probably heard that FAFSA is changing this year. (It is. A lot. It won’t be settled until “December.”) So we’re waiting to update this section of the guide until things settle down and we’re certain there are no more surprises.

In the meantime, here’s a comprehensive, searchable guide Amanda’s already made to go over all the changes we know about.

Here are a couple highlights:

“Expected Family Contribution” (EFC) is now “Student Aid Index” (SAI). New name, same function.

Why is this my first highlight?

Because if you’re searching on the web to learn about FAFSA or to learn about how colleges are awarding aid and see “EFC”, that’s code for “this site hasn’t been updated to reflect the changes to the new FAFSA and you should either reach out or check back later.”The Pell Grant (up to $7,400 in free money you could get for filling out a FAFSA) is available to way more people than ever before. Check out Amanda’s “Am I Eligible for a Pell Grant? Cheat Sheet” Chart to see if you’re definitely getting money.

The folks at Federal Student Aid are churning out tons of great resources to create hype. (Good on them.) Start here to find any additional information you need. Or if you prefer snappy 1-3 minute videos to explain the basics, check here.

Happy FAFSAing!

– Amanda and the College Essay Guy Team

What is FAFSA?

FAFSA stands for Free Application for Federal Student Aid. As the name suggests, it’s a free online form that you (likely with your parent’s help) need to fill out every October in order to qualify for federal aid for the following school year.

The FAFSA contains about 100 questions (give or take) but don’t let that get you down—it usually takes less than an hour to complete. (My personal record is 12 minutes.) And good news: the FAFSA is decreasing the number of questions considerably for 2023-2024.

And here’s why the FAFSA is a key piece of paying for college:

The FAFSA is used by some states and the vast majority of colleges to determine how much and what kinds of need-based aid you’re eligible for. So I’m glad you’re here.

Quick note on eligibility: If you are not a US Citizen, check here to see if you’re an eligible noncitizen for FAFSA purposes. Please note that some states offer alternative financial aid applications for undocumented students who may be eligible for state aid (for example, New Jersey’s Alternative Financial Aid Application).

There are two categories of aid under the financial aid umbrella: gift aid and self-help aid.

Gift aid comes in two forms:

- scholarships (merit-based aid)

- and grants (need-based aid)

These are equally powerful and awesome, as both are types of money you don’t have to pay back!

We spent a whole section on scholarships (see section 1). They can be a bit confusing to track down but are fantastic when they pay off.

Grants, on the other hand, you don’t have to hunt for: they are almost entirely funneled through only a few forms, the most notable of which is the FAFSA. (The other forms, like the CSS Profile and state aid forms, will be tackled in section 3.3.)

The other kind of aid—self-help aid—includes loans and work study. These are also, while less glamorous, incredibly helpful and, you guessed it, determined by the FAFSA.

While scholarship awards depend on how awesome you are in some way—getting good grades, playing a sport, writing an essay, making a prom dress out of duct tape—grants depend solely on how much your family can afford to pay for college.

How do they determine how much my family can afford?

There’s a federal formula (a secret blend of 21 herbs and spices kinda’ deal) that takes all the info you put into your FAFSA—income, assets, family size, parent age—and distills it down to one number, currently called an EFC (“Expected Family Contribution”), but that’s changing to SAI (“”Student Aid Index”) starting fall of 2022 when the FAFSA gets a much needed makeover. The federal government, state governments, and colleges use that number to determine who needs money the most, and how much they get.

This six-digit number is super important, and you only find yours out after completing the FAFSA. (We’ve got a whole section on this here (3.2).)

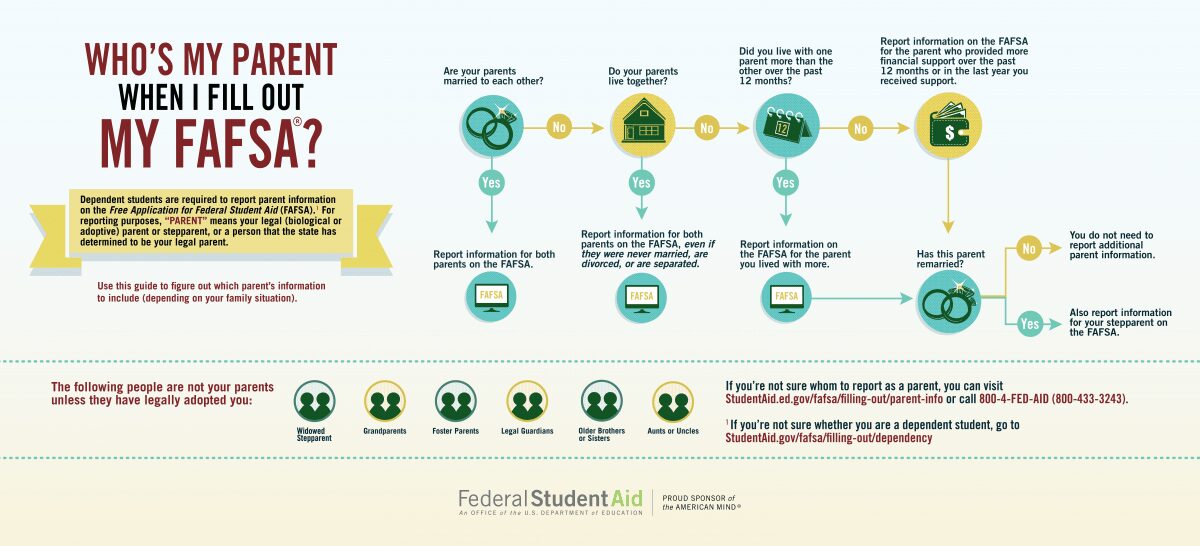

Who is my FAFSA parent?

To answer this, we’ll start with the simplest cases and build into the more complex.

Students living with both parents:

(whether biological—married or unmarried—or those who legally adopted you before you turned 13) are welcome to skip ahead to “Action Steps!” below.

Students living with only one parent because:

your parents never married

or they are divorced/separated and only one has custody of you

or one has unfortunately passed away (in which case, please be sure to get the support you need)

you can also skip ahead to “Action Items” below.

Students living with one parent sometimes and the other parent sometimes:

If your parents are divorced and split custody, the parent you live with most of the time is your parent for FAFSA purposes.

If your parents split custody evenly, then the follow-up question is “who provides more financial support?” If it’s a 50/50 toss up again, then most students err on the side of the parent whose financial information will benefit them more, i.e. the parent with the lower income. It doesn’t matter who “claimed you” on their taxes; however, if you do opt to have as your FAFSA parent the parent who didn’t claim you as a dependent on their taxes for the year the FAFSA asks about, then you’ll likely be flagged for verification, an annoying but harmless process that we cover in Section 3.3.

One final important note for children of divorced parents trying to navigate this whole thing: if your FAFSA parent remarried, then you’ll include that step-parent’s financial information as well.

Students not living with either biological parent:

If you don’t live with either of your biological parents, but another adult legally adopted you, then that’s the parent you use.

If you weren’t adopted but an adult you live with has been granted “legal guardianship” by a court, then you’ve hit the financial aid jackpot, since you don’t need anyone’s info but your own and you’re guaranteed maximum federal aid!

If you don’t live with either of your parents and haven’t been adopted by or entrusted in legal guardianship by a court to the adult(s) you live with, you still have to use your biological parent’s information.

This sucks for some students because you may not know where this person is or may not feel safe contacting them. If this is the case, you can still complete the FAFSA without their information by completing the form as an independent student. This can be dicey though, because—unless you can answer “yes” to one of the 10 dependency questions—you likely won’t be awarded grant aid, only lots of loans. You can contact colleges to rely on what’s called “professional determination” aka the mercy of their financial aid office. Hopefully, this element of the FAFSA will change for the better when the FAFSA gets remodeled in 2022 for those in college Fall of 2023 and onward.

Important note for unaccompanied students: if you can answer “yes” to the final dependency question about homelessness, make sure you’re designated as “McKinney-Vento” by your high school’s McKinney-Vento liaison—ask your counselor, they’ll know who this is and it’s completely confidential—before you graduate high school to ensure you don’t have to use your parent’s info for FAFSA at any point, and will are more likely to receive non-loan financial aid.

Even more details about who to report as your FAFSA parent can be found here, including what to do if you’re a citizen but your parents are not. Hint: you’re still eligible for federal aid and should still fill out the FAFSA.

In the next section, I’m going to walk you through the FAFSA. Scary? Maybe. Boring? Not to me, but maybe to you. Difficult? Hopefully not. Doable? Definitely. 🙂

But before we tackle this form, there are two incredibly helpful things you can do in advance to make your life so much easier.

[action_item]

Action Item: Create a FSA ID

Now that you know who your FAFSA parent is, he/she/they (to clarify, only one is needed, but I’m adding “they” if that’s the pronoun they use) and you can create your own Federal Student Aid usernames and passwords.

Here’s the website.

One FAFSA Parent creates his/her/their own FSA ID … AND you create your own FSA ID. If your parent already has one from filling out the FAFSA for a sibling/themselves, then they use the same one they already have.

Each of you must use different email addresses.

Because you’ll want to complete a FAFSA again for each year you’re in college (including graduate school!), and this username/password combo will not change year-to-year, make sure you don’t use an email address—like one assigned by your high school—that you won’t have access to after you graduate high school.

Important note: All FAFSA related websites should end in “.gov” and you’ll use your FSA ID for taking out and managing federal loans at some point. So it’s SUPER important you don’t share the login information (duh) and keep the username/password you create in a place you can find it again (also duh, but you’d be amazed how often I sit patiently while folks scramble to locate their login info so I can help them with their FAFSA.)

When should I create my FSA ID?

The ideal time frame is about a week before you start the FAFSA, but this can be done at any point. If you have both your and your parent’s FSA IDs ready to go before you begin filling out the FAFSA the process will go quicker as logging in with it auto fills some questions and you don’t have to wait for the Social Security Office to process your ID in order to sign the FAFSA at the end.

[action_item]

Action Item: Get Prepared

1) Download/print the Stuff I Need for FAFSA Checklist.

2) Get your FAFSA parent a copy of that checklist too.

3) Set a date by which everything will be gathered and you and your FAFSA parent can sit down (maybe over a favorite snack) and take about 30 minutes to secure between $5,500 and almost $12,000 to help pay for college. (That’s $183 to $400 per minute!)

Once you’re all set, move on to the next section to tackle the FAFSA!