What is a financial aid award letter?

It’s a list of all the different kinds of money—scholarships, grants, loans, work study—you’ve received to go to a particular college next year.

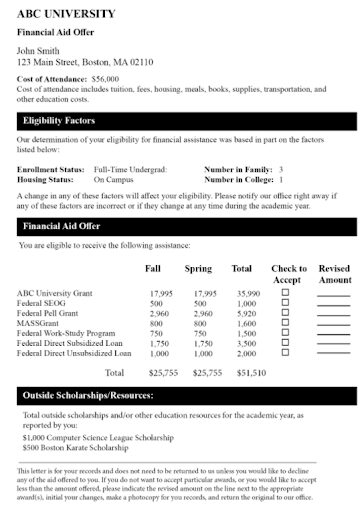

It may look something like this….

Or this…

Or maybe this…

Every college you are accepted to creates one of these for you.

Why is it a big deal for me to find and understand my award letter?

Imagine shopping online for a set of headphones.

Now imagine choosing which pair to buy and having no idea how much they cost. They could be $10. They could be $5,000.

That would be silly. Cost is a key part of any purchasing decision.

Now imagine that the average cost of a set of headphones was $10,000, but could range from $2,000 up to $55,000. And—in this crazy scenario we’ve constructed—once you buy a set you have to buy a new pair every year for three more years.

In these circumstances, choosing a pair price-blind would be downright dangerous. You could be signing up for no debt or $220,000 in debt before you even turn 20! With too much debt, there goes any hope of affording a car, a house, a wedding, or a vacation for about a decade.

Boo sauce.

This is why knowing the price in advance is so important and how your award letter can help you make an informed decision.

Your financial aid award letter is a roadmap to the next 10+ years of your financial life. Even though it may seem intimidating to read and understand—perhaps because it’s your first official financial document as a full-fledged adult—the consequences of not doing so are even more intimidating!

How do I find my award letter?

Award letters are either mailed to you via the postal service or made accessible via your accepted student portal. If it’s on your student portal, you should have gotten an email telling how to access it.

When should I expect to receive my award letters?

Anytime after you’ve been officially accepted to the college: typically December through February.

I’d start to worry if you haven’t seen one by the end of March.

If this is you, don’t stress too much. Just take action. Call/email your college’s financial aid office to find out what the possible hold up is.

The single most common reason a financial aid award letter isn’t generated is that there is a problem with the student’s FAFSA. Here are the top three FAFSA hiccups and how to fix them.

#3 FAFSA (or CSS Profile) was never submitted.

Whoops! Go back to Section 3 for help filling these out ASAP! Usually the issue has to do with missing signatures.

#2 The college wasn’t added to the FAFSA.

This is an easy fix. Log in to your FAFSA form using your FSA ID. Click “Make a Correction.” Go to the School Selection page. Add the college you forgot. Go to the submit page and sign using your FSA ID. Have your FAFSA parent do the same. Hit submit. Wait 5 days. Check with the college again.

And the #1 most common reason an award letter is delayed is you haven’t checked your email.

If a college is missing anything they need to finish processing your award letter, they would have emailed you about it. Probably multiple times.

If you haven’t gotten any such email (and you’re sure you’ve checked the correct email address and your spam/junk folders), then call or email the financial aid office to politely ask what the holdup is. Feel free to use the template below.

Hello,

My name is ____. My student ID is [insert assigned college student ID]. I was accepted to attend college at your institution in the fall. I’m emailing to inquire about the status of my financial aid award letter as it does not appear in the student portal and I haven’t received a digital or physical copy yet.

Please let me know if you are missing any items from me. I’ve checked my email and student portal but haven’t seen anything to indicate that my award would be delayed.

If all is well, please let me know—at your convenience—when I might expect to receive the award letter.

Thank you for your attention, and I look forward to making my enrollment decision once I’ve had a chance to review my financial aid package.

Who do I contact if I can’t find my award letter?

Google the name of your college followed by “financial aid office staff.” That should direct you to a whole list of folks. I’d advise not contacting the “Director of Financial Aid.” I’d go for a “counselor” or “administrative assistant” to start out with as they can usually direct you to the exact person you need to talk to.

And remember, you’re already accepted! The people on the other end are paid to help you with this exact process. Think of it like contacting customer service. 🙂

Pro Tip: I know your generation is far more comfortable with an email, but from experience I can tell you that calling is way more helpful. You get an answer faster by talking to a real person. Plus, he/she can answer any follow-up questions then and there to eliminate any confusion and ratchet down your stress levels.

[action_item]

Action Item: Find at least one of your financial aid award letters. Once you’ve found one, take a picture or screenshot of it and save it to a safe place on your computer or phone so you can find it again whenever you need it.

Once you’ve got one or more of your award letters handy, we can move on to making sense of the numbers.

How do I make sense of my award letter?

Wouldn’t it be nice if you could just stick all the numbers from your award letter into a special calculator and it would give you the bottom line of what you have to pay?

You can.

We made this handy spreadsheet just for this purpose: Amanda’s Award Letter Analyzer.

It looks like this:

Here’s how it works:

Match the names of things on your award letter to the categories on the analyzer.

Input the amounts.

Add and subtract as directed.

Compare across colleges to make an informed decision about where to attend and how much it will actually cost.

Are you ready?

Snag one of your award letters and let’s walk through this step-by-step.

Direct Costs

1. Jot the name of the college in the top row.

2. Look to see if your award letter lists the college’s direct costs: tuition, fees, room and board (aka housing and meal plan). Fill these in.

If the costs aren’t listed on the award letter, google “[name of college] cost of attendance” do your best to find the numbers for the upcoming school year.

If you can only find this year’s, that’s fine. Just know costs usually increase by 2-4% each year.

For public universities, make sure you look up the in-state or out-of-state rate, whichever is appropriate.

Anyone who’s been on a college tour has heard about all the “free” stuff you get at college: free workout facilities, free events, free ice cream and pizza at those events, free personal and career counseling, free tutoring, free laundry.

Yeah. That stuff isn’t free. It’s included in “fees.” You’re paying for it so you may as well make the most of it!

Most fees are required. Some additional ones can be added (parking pass, visits to the health clinic, damage to college property). And one in particular can usually be dropped.

Pro Tip: If your folks already have you on their health insurance, you can opt out of the plan your college may have automatically signed you up for. This can save a chunk of change.

More About “Room and Board”

If you plan to live at home, you can write $0 for room and board, though you may want to talk to your parents to make sure they won’t charge rent!

If you plan to live off campus, you can write $0 here too, but you’ll still need to consider how you intend to pay for rent and groceries which will triple to quintuple–think NYC–your indirect costs (at the bottom of the sheet).

If you plan to live on campus, check to see the different rates for different housing options and meal plans. Adjusting to a cheaper option can be a great way to lower costs. But for right now, let’s stick with calculating based on the average.

3. Add “Tuition & Fees” and “Room & Board” together and put the total in the “Total Direct Costs” line. This is the total cost the college is charging for your first year of attendance.

Example:

Those are some big numbers. Let’s see how much we can whittle them down with some free money.

Gift Aid

4. Check your award letter for federal grants. Look for the words “Pell Grant” and “SEOG” or “Supplementary Educational Opportunity Grant.” Total these and jot them on this line. If you don’t see either of these, write $0. Note: The amount should typically be the same for each school.

This is money you received from the federal government because you filled out the FAFSA and the algorithm determined that you fall into the “Yeah… You look like you could use some help” category. This money will follow you to whichever college you choose (and consequently should be the same on every award letter.)

You can continue to get this money every year so long as your financial situation remains about the same and you fill out the FAFSA each year you’re in school for up to four years.

If you did the FAFSA and your Student Aid Report showed that you were awarded a Pell Grant, but it’s not showing up on your award letter, something’s up and you need to contact your college’s financial aid office ASAP.

5. Look for anything with the name of your state in it. This is probably a state grant or scholarship you’ve been awarded because you are attending college in your home state. Jot the amount on the line.

You received this money for one of three reasons: you filled out the FAFSA, you filled out a state-specific form, or your state offers an automatic scholarship based on GPA, test scores and/or class rank. Your high school or financial aid counselor will know. Whichever of these reasons it was, just make sure you understand how you can continue to receive the funds after this year.

6. Look for anything with the name of the college in the description. Anything else that says “grant” or “scholarship” can be added into this line.

7. If you’ve received any outside (online or local) scholarships that you know can be applied at this school, plunk those right here.

8. Add up everything in the Gift Aid column for this school and write the total here.

Example:

Note: I’ve added descriptions in parentheses, but you don’t need to do that in yours.

Net Costs

Now, for our first really important calculation: take the Total Direct Costs and subtract the Total Gift Aid. This is your Net Cost: how much you’ll actually be paying for your first year of college.

I freely admit that “Net Cost” is technically defined in financial aid to include indirect costs which we’ll talk about in a second. These usually add up to $2,000–$5,000 extra.

I tweaked our definition of “Net Cost” here for two reasons:

- For most students, these costs vary only slightly by the time they’ve narrowed down to the final few schools. If your student has two in-state colleges and one college an entire continent away, I’d definitely revert to the normal way of discussing “Net Price” in order to make a fair comparison.

- Students and families typically like to have a clear picture of the “bill” from the college which includes only direct costs. I’m a fan of clarity.

This said, please forgive me, almighty financial aid gods—and Jeff Levy—for messing with the rules.

So for this rando student, Fancy Private College will cost $5,500, Flagship State U will cost $6,500, and ABC University is a whopping $10,655 despite having the lowest direct costs!

[action_item]

Action Item: If you’re following along, take a look at your Net Cost.

Is this a happy, manageable number? Awesome. You still need to think about indirect costs. Scroll down to the money-grubbing Santa and read on.

Is this number not-so-happy? You have some options.

What can I do if my Net Costs are too high for my family and me to pay right now?

If you’re wondering how to lower the Net Cost, the preferred way is to increase your Gift Aid through outside scholarships or even negotiating with the school (see this super helpful post on financial aid appeal letters).

If that ship has sailed, then you won’t really be able to lower your Net Cost unless you opt to live at home. (Be careful about choosing this option though, as some colleges will decrease your aid if you change from living on campus to off campus.)

But don’t despair! You can give yourself some breathing room to come up with the missing funds by taking out loans.

Just for filling out the FAFSA, you are guaranteed $5,500 in loans for your freshman year.

Loans

9. Look at your award letter for either a $5,500 Unsubsidized (“Unsub”) Loan or a $3,500 Subsidized (“Sub”) Loan and a $2,000 “Unsub” Loan.

You may even have some other split of the subsidized and unsubsidized loans, but they always add up to $5,500 for dependent students. (If you’re independent, you’ll get an extra $4,000 in unsubsidized loans for a total of $9,500.)

Jot these loans into your analyzer. They should be the same for every college.

What is the difference between a subsidized loan and an unsubsidized loan?

Put a little happy face next to the subsidized loan. This is a loan that the federal government pays the interest on for as long as you are enrolled so the amount doesn’t grow.

Next to the unsubsidized loan, put a little “meh” face. This is a loan that accrues interest (gets bigger) while you’re in school. The good news is that it usually has a reasonable interest rate and, just like the subsidized loan, you don’t need to start paying it off until you are 6 months out of college. This could be after you graduate with your bachelor’s degree, after you finish your PhD or when you decide to “take a year off”. Yep, loan payments kick in after you cease to be enrolled at least half-time in college for 6 months.

What You Need to Know About Student Debt in Under 30 Seconds

If you take out the maximum federal loans each year, you’ll be over $27,000 in debt by the time you graduate. This is about the national average. I wouldn’t advise taking on much more for a bachelor’s degree, especially if you plan to go to graduate school or enter into a typically lower paid profession like teaching or social work.

See that line for “Other Loans”? It is possible for you to take out private loans from a bank, but this is generally inadvisable due to the high interest rates. If you’ve got a wealthy relative willing to lend to you on good terms, then great! Otherwise, we do our best to leave this line blank.

Estimated Bill

Net Cost is how much you will eventually pay for your first year of college. But how much do you actually have to pay to the college before you start classes in August? This is where the Estimated Bill comes in.

10. Take Net Cost and subtract the Loans. This is your Estimated Bill. This is how much you and your family will need to come up with out-of-pocket for your first year.

You can also arrange a monthly payment plan through your college to spread out the costs a bit more. Just be sure to set it up in June instead of August so you don’t have 3 months due at once!

The Odds and Ends: Work Study, PLUS Loans, and Indirect Costs

There may be a few other pieces of information on your award letter that haven’t found a spot yet on the analyzer. Let’s tackle those now.

Additional Financing

Sometimes Gift Aid and Student Loans just aren’t enough to cover the bill. You do have some other options to make the numbers work.

Parent PLUS Loans

If you see “PLUS Loan” on your award letter, add it to your analyzer.

One easy way to bridge the gap between what your family can afford and what you’ll need to pay is to ask your parents about their willingness to take out PLUS Loans.

PLUS Loans are federal loans offered to your parents so they can help you pay the rest of the Estimated Bill.The good news is that unless your parents have truly terrible credit, they are likely to be granted a loan for as much as you need. However, even if your award letter lists a PLUS loan, the loan is not guaranteed until your parent actually applies and is approved for it.

PLUS Loans are easy to obtain but they are also incredibly dangerous if used irresponsibly.

I generally advise taking PLUS Loans only after you’ve maxed out the federal student loans because the PLUS loan interest rates are always higher than the student loan rates. (For example, the 2020-2021 Federal loan interest rates were 4.53% for Parent PLUS loans versus 2.75% for student loans.)

Also, I advise against taking out more than a few thousand dollars in PLUS Loans as it’s very easy for your family to become overwhelmed in debt. Remember, the loan amount you list on your analyzer is just for one year. Times it by four and add some interest and that’s the amount your family is signing off to make payments on every month from now until—typically—10 years after you graduate college.

Finally, if your family does need to take out additional loans, it may be worth considering other options like a home equity loan—but that also comes with caveats, since interest rates can vary, and a HELOC may be dangerous for lower-income households. So it really depends on your family situation and the current interest rates.

Work Study

If you see “Work Study” on your award letter, jot it in. The usual amount is $2,000-$3,000.

Work study is, as you may know, the option to take an on campus job. At some schools, these jobs are a sure thing, while at others, you have to find and apply for them before they fill up.

What many folks don’t realize is that the amount (in the majority of cases) is not applied as credit toward tuition, but instead is just like a normal job in that you are paid biweekly through direct deposit to your checking account. That’s why we’ve counted it separately from your gift aid even when your college lumps it all together. (Adding work study to the gift aid kinda makes the college’s award letter look more generous than it is, IMHO.)

You can use any money earned from work study for all the indirect expenses you will have. This is why we don’t add it into your Net Cost or Estimated Bill calculations: because you rarely actually hand that money over directly to the college. That said, you can certainly save up your earnings and use them to pay for the bill! Regardless of whether you were offered one of these work study jobs, you can always get a job off campus to help cover your indirect college costs.

Work Study, an off-campus or summer job and savings are all great ways virtually all college students cover the costs of college that aren’t included in their bill.

And what costs are those?

Indirect Costs

Textbooks, obviously, are one, though some colleges are pushing for virtual materials.

Pro Tip: OMG don’t buy new books from the bookstore! Rent, borrow from the library or buy used copies!

Probably a nice new laptop or device of your choice (though at many four-year colleges you can get away with using the publicly available computers).

What about gas money or plane tickets to get to and from campus every Christmas and summer when the dorms close?

And Command Strips and sheets for that dorm room?

And I think your roommate would appreciate it if you keep toothpaste and deodorant in supply.

Every Starbucks study session and movie with friends adds up.

Plan on $2,000 at each school if you’re thrifty, $5,000 or more if you’re not.

The primary difference between schools here is the transportation costs: farther means a plane ticket, closer means resisting the temptation to burn gas coming home every weekend. And commuters, consider not only gas, but also if you’re really going to pack your lunch every class day when considering your food costs.

Honeybuns and Gatorade. Breakfast of Champions.

Making Your Final Informed Decision

Once you’ve filled in the analyzer using the award letters from each of your colleges, it’s time to make some final decisions.

The easiest way to compare schools’ affordability is to look at the Net Cost for each.

Schools within $2,000 of each other are basically the same in the long run and the difference in cost shouldn’t really sway you towards one school over another.

If you strongly prefer a school that is within $5,000 of another lower offer at a comparable school, you might consider asking that college you like more if they can match the other school’s offer. (Check the college’s website to see if they explicitly say they won’t negotiate award letters before attempting this.) The worst they can say is “no.” We’ve written a whole blog post about how to rock this appeal process. Check it out here. There’s also a ridiculously helpful website dedicated to walking you through the process.

Have you picked a school? Give yourself a couple days to think it over, but don’t miss that May 1 decision deadline! They will give your spot away if they don’t hear from you!